The cost center and cost center accounting

How can companies keep their costs under control in 2026 while simultaneously increasing efficiency? The answer often lies in targeted management and control of expenses.

A cost center is the central tool that modern companies use to achieve transparency, efficiency, and control in cost management. Anyone aiming for sustainable business success cannot avoid a clear structuring of costs.

Do you want to know how cost centers optimize business processes? Here you’ll get a comprehensive guide: from the definition through types and structure to practical tips for implementation and current trends. Gain clarity and control over your company’s figures!

What is a cost center? Definition and fundamentals

Cost centers are a central element of modern accounting. Companies use them specifically to record costs transparently and manage them in a targeted manner. But what exactly is behind the term? In the following sections, you’ll learn everything important about the definition, distinctions, and practical areas of application.

Basic definition and significance

A cost center is an organizational unit in the company in which costs are recorded in a targeted way. These can be departments such as production, sales, or administration. The cost center forms the basis for cost and performance accounting and is indispensable for structured accounting.

In contrast to other terms, such as cost object (the product or service) or cost type (the type of cost, e.g., materials), the cost center describes the place where costs arise. Over the decades, the approach has continuously evolved and is more relevant than ever in 2026. Companies benefit from clear cost centers to better manage expenses and create transparency.

If you want to delve deeper into the technical fundamentals, you’ll find a solid definition and tasks of cost center accounting in the Fundamentals of cost center accounting.

Distinction: Cost center vs. cost object

The cost center represents the place within the company where costs are incurred. The cost object, on the other hand, is the item to which the costs are ultimately assigned, such as a product or a service.

Examples to distinguish:

-

Production is a cost center because costs arise here

-

The manufactured car is the cost object, since the costs are assigned to it

In practice, cost center and cost object accounting interact. Controlling uses both systems to monitor the profitability of individual areas and products. This makes it possible to trace where costs arise and how they are distributed.

Typical areas of application

Cost centers are used in almost every company. Typical cost centers include, for example:

-

Departments such as Sales, Administration, or Research & Development

-

Locations and branches

-

Projects and temporary teams

The definition of a cost center is flexible and depends on size and industry. Small companies usually use a few clearly delineated cost centers, while large corporations build complex structures with numerous units.

Regardless of company size, cost centers enable targeted cost control and promote efficient processes. They are therefore a key element for transparency and steering in modern management.

Types of cost centers and their structure in the company

The selection and structuring of the various cost centers is a central element for transparency and control in the company. Depending on the setup and business model, different types are distinguished, each fulfilling specific tasks and functions. A clear classification helps assign costs precisely and manage the profitability of individual areas in a targeted way.

Main cost centers, secondary cost centers, and auxiliary cost centers

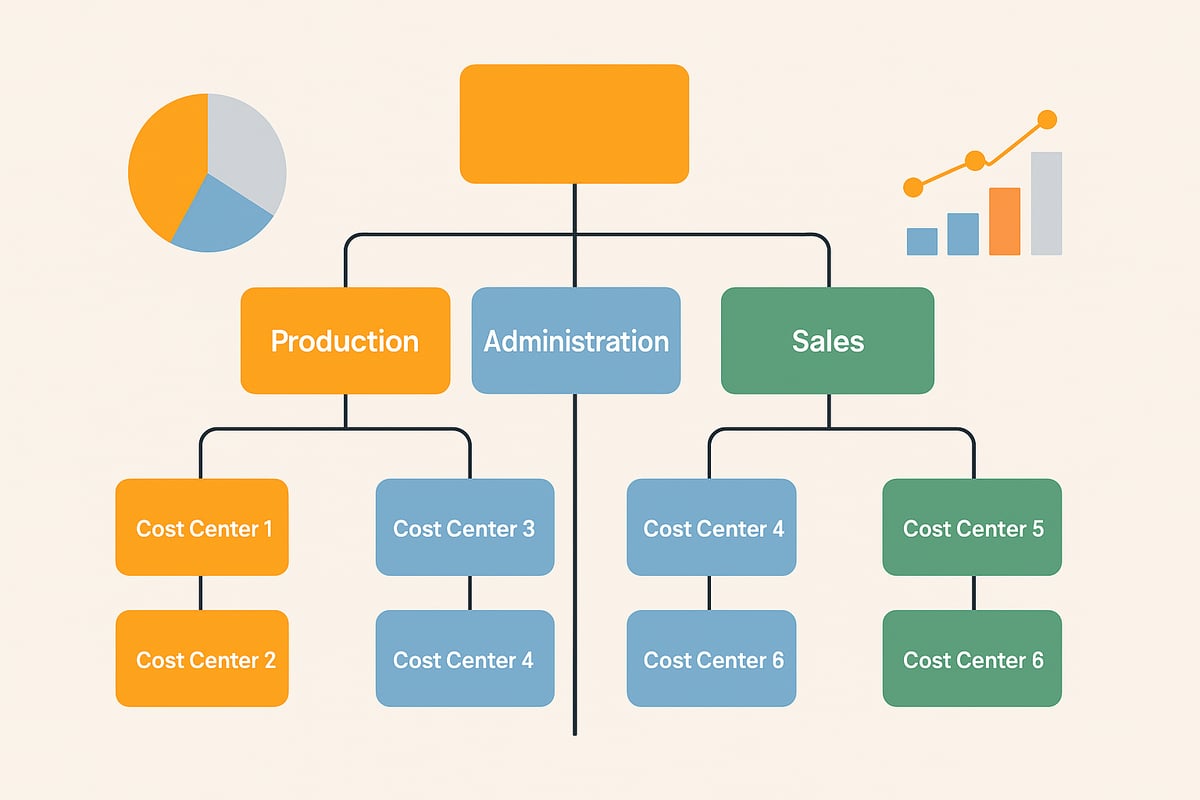

In every company, cost centers can be subdivided according to their contribution to value creation. Main cost centers are areas that are directly involved in the creation of products or services, such as production or sales. They contribute significantly to the company’s performance.

Secondary cost centers handle tasks that run independently and separately from main production, such as waste disposal or an in-house warehouse. Auxiliary cost centers, on the other hand, support the main processes, for example through IT, the cafeteria, or a repair shop.

Examples of types of cost centers:

-

Production (main cost center)

-

Waste disposal (secondary cost center)

-

IT department (auxiliary cost center)

This distinction makes the analysis and control of costs significantly more efficient.

Additional types of cost centers: project and temporary cost centers

In addition to the classic structures, there are project-based and temporary cost centers. Project cost centers are set up for individual, time-limited initiatives, such as major IT projects or construction projects. They allow for targeted control and post-calculation of the expenses incurred.

Temporary cost centers often arise for special promotions, events, or campaigns. They are dissolved again after the project or event has been completed.

Advantages of project-based and temporary cost centers:

-

Clear cost assignment for projects

-

Better tracking and analysis

-

Flexible adaptation to company needs

With these cost centers, the company remains agile and can respond to changing requirements.

Functional, spatial, and organizational structuring

The structuring of cost centers follows various criteria. Functionally, it is oriented toward core tasks such as procurement, production, administration, sales, or research and development. From a spatial perspective, cost centers can be distinguished by locations, plants, or branches.

Organizational factors also play a role: responsibilities are clearly assigned, so that each cost center is managed by a head or responsible person.

Typical classification criteria:

|

Classification |

Examples |

|---|---|

|

Functional |

Production, Sales |

|

Spatial |

Plant I, Berlin branch |

|

Organizational |

IT team, project group |

This creates a clear structure that provides the company with orientation.

Practical examples and infographic on cost center structure

In practice, the importance of a structured cost center is particularly evident in industry, the service sector, and administration. Industrial companies often work with complex hierarchies, while service providers use flexible project cost centers.

A clear cost center plan simplifies administration and reporting. Modern tools and digital solutions help manage processes around the cost center efficiently. Those specifically interested in optimization will find practical approaches in the area of Management of business processes.

A clear structure and regular review of the cost center hierarchy are crucial for sustainable business success.

The cost center plan: structure, creation, and best practices

A clearly structured cost center plan is the backbone of effective cost management. It provides an overview, ensures transparency, and forms the basis for precise cost control in your company. But what does a modern cost center plan look like in 2026, and what should you pay attention to when creating it?

Structure and content of a cost center plan

A cost center plan is a structured overview of all cost centers within a company. Each cost center is clearly identified by a number and a clear designation. The classification is usually by functional areas such as production, administration, or sales.

Important details on the cost center sheet are:

-

Name of the cost center

-

Numbering system (e.g., 1000 = Production)

-

Description of tasks

-

Responsible person

-

Date established

A tabular structure ensures transparency and enables quick retrieval of each cost center. Modern companies rely on digital solutions to adjust the plan flexibly and manage it efficiently.

Creating and maintaining the cost center plan

The development of an individual cost center plan begins with an analysis of the company structure. In the next step, the relevant cost centers are defined and responsibilities assigned. The numbering should be logical and comprehensible so that each cost center can always be clearly identified.

For administration, it is advisable to use accounting software to implement updates and adjustments efficiently. Tools for automation of accounting help keep the plan up to date and avoid errors. It is important that the plan is reviewed regularly and adapted to changes in the company.

Benefits of a structured cost center plan

A well-organized cost center plan facilitates cost control and supports budget planning. Each cost center can be monitored and analyzed in a targeted way, creating transparency for management.

Typical benefits include:

-

Rapid identification of cost drivers

-

Better traceability of expenditures

-

Efficient allocation of budgets and responsibilities

Examples from practice show that companies with a clear cost center plan respond more flexibly to market changes and can sustainably optimize their cost structure.

Cost center accounting: process, methods, and practical implementation

The cost center is a central instrument when it comes to the precise management and control of overheads in the company. It helps create transparency and makes the profitability of individual areas measurable. But how does cost center accounting work in detail, and how can you use it efficiently in 2026?

Objective and tasks of cost center accounting

Cost center accounting aims to allocate all overhead costs to the respective cost centers based on causation. This reveals where costs actually arise in the company and how economically individual areas operate.

An important aspect is the formation of calculation and overhead rates. These enable the onward allocation of overheads to products or services. This allows those responsible to initiate targeted optimization measures and plan budgets more effectively.

A well-thought-out cost center accounting system therefore provides transparency, control, and targeted management of corporate resources. With clear responsibilities and a comprehensible structure, efficiency in cost management increases noticeably.

Process of cost center accounting

The typical process of cost center accounting begins with cost type accounting. Here, all cost types in the company are first recorded and assigned to the appropriate cost centers.

In the next step, primary costs, i.e., directly attributable overheads, are allocated to the respective cost centers. This is followed by the internal allocation of services between auxiliary and main cost centers. This so-called secondary cost allocation ensures that supporting areas such as IT or maintenance are charged based on causation.

A central tool is the Betriebsabrechnungsbogen (overhead cost allocation sheet), which maps all steps in a table. A clear explanation of the structure of the Betriebsabrechnungsbogen helps you understand practical implementation and avoid errors.

Methods and allocation keys

There are various methods for allocating overheads to cost centers. Direct allocation is used when costs can clearly be assigned to a cost center, for example electricity costs based on consumption.

Indirect allocation uses allocation keys such as floor space, number of employees, or machine hours. In this way, costs are distributed proportionally across several cost centers. Choosing the right key is crucial for the meaningfulness of cost center accounting.

|

Method |

Example |

Advantage |

|---|---|---|

|

Direct allocation |

Electricity meter per cost center |

Precise assignment |

|

Indirect allocation |

Allocation by floor space |

Flexible, cross-industry |

Careful selection and regular review of allocation keys ensure that cost center accounting remains meaningful.

Software and digital tools for cost center accounting

Digital tools play an increasingly important role in 2026 for managing cost centers. Modern accounting and ERP systems enable automated allocation of costs, real-time evaluations, and integration with other corporate areas.

The advantages are obvious: fewer sources of error, faster evaluations, and better traceability. Dashboards and reports make developments visible and facilitate management. For growing companies in particular, the use of digital solutions is a crucial competitive advantage.

By combining cost center accounting with digital controlling, processes can be made more efficient and optimization potential identified at an early stage.

Cost centers in controlling: benefits, KPIs, and optimization potential

Cost centers are the backbone of cost control in companies today. A well-thought-out cost center management approach makes the difference between mere number administration and real steering. By analyzing individual areas in a targeted way, costs can not only be recorded but also actively influenced.

Importance for controlling and corporate management

The cost center is a central tool in controlling because it brings transparency to the cost structure. This allows those responsible to plan budgets in a targeted way and monitor expenditures. By clearly assigning costs to each cost center, potential savings quickly become apparent.

Each cost center often has its own area of responsibility. This decentralizes the control of expenditures, and department heads can independently take optimization measures. So, anyone who has their cost centers under control not only manages the budget but also actively shapes the company’s future.

Key metrics and analyses

In controlling, reports on each cost center provide important decision-making foundations. Typical metrics include costs per cost center, budget variance, and the comparison of actual to planned costs. Dashboards and graphical evaluations make trends and anomalies immediately visible.

With the help of digital tools, these reports can be created and evaluated automatically. Modern solutions such as solutions for financial controlling simplify analysis and help identify cost drivers. This keeps each cost center in view and makes reporting more efficient.

|

Metric |

Meaning |

Example |

|---|---|---|

|

Costs per cost center |

Determination of costs per area |

€100,000 Sales |

|

Budget variance |

Difference between plan and actual |

+€2,500 |

|

Cost trends |

Development of costs over time periods |

-5% compared to the previous year |

Practical tips for optimization

To fully leverage the potential of each cost center, it is advisable to regularly review the cost center structure. This avoids overlaps or double postings. Best practices include a clear definition of each cost center as well as clear responsibilities.

Involving employees in cost control also fosters cost awareness. Benchmarking between similar cost centers can reveal additional optimization opportunities. If you follow these tips, the cost center becomes a real success factor in the company.

Guide to the practical introduction and management of cost centers

Anyone who wants to introduce cost centers in a company needs a clear roadmap. Without structure and clear responsibilities, cost management quickly becomes confusing. With a systematic approach, the rollout of cost centers succeeds efficiently and in a future-proof way.

Step-by-step guide to implementation

Start with an analysis of the company structure. Where do costs arise, which areas are relevant? Next, appoint those responsible for each cost center. This clarifies who is in charge of cost monitoring.

Then create a clear cost center plan. A clear hierarchy and numbering help here. Afterwards, choose accounting software that supports the management of your cost centers. Many companies use the integration with Lexware Buchhaltung to automate data flows and minimize errors.

Finally, train your employees. Only those who understand how to work with cost centers can use them effectively. Regular adjustments ensure up-to-dateness.

Checklist for implementation:

-

Analyze company structure

-

Define responsibilities

-

Develop cost center plan

-

Select and integrate a software solution

-

Train employees

-

Ongoing review and adjustments

Key success factors and common pitfalls

Successful cost center management stands and falls with clear definitions. Each cost center needs clear boundaries; otherwise, overlaps and unclear responsibilities threaten.

Select suitable reference bases for cost allocation, such as headcount or floor space. But don’t overdo the level of detail: too many cost centers increase effort and complicate control.

Avoid common mistakes such as double postings or missing responsibilities. Especially in public administration, there are helpful resources such as the guide to cost and performance accounting, which offers practical tips for managing cost centers.

Common pitfalls:

-

Unclear delineation of cost centers

-

Missing or duplicate responsibilities

-

Overcomplicated structure

-

Inadequate communication within the team

Examples from business practice

Many companies report significant improvements after introducing a structured cost center approach. In medium-sized companies, the clear assignment of costs led to more transparency and faster action in controlling.

Large companies use cost centers to manage budgets in a targeted manner and identify savings potential. In practice, regular review and adjustment of the cost center structure proves to be crucial.

Success factors from practice:

-

Involvement of all relevant departments

-

Continuous optimization of the cost center structure

-

Use of automated reports and dashboards

In this way, the cost center becomes an effective management instrument—whether in a small business or a multinational corporation.

Current trends and developments in cost center management 2026

Digitalization is fundamentally changing cost center management. More and more companies are relying on automated processes to manage cost centers more efficiently. Digital tools enable fast data capture and analysis. At the same time, the importance of cloud solutions is growing, as they offer flexibility and make cross-location work easier. This makes the management of a cost center more transparent and less error-prone.

AI, data analytics, and new types of cost centers

Artificial intelligence and data analytics are key drivers of cost center management in 2026. Smart algorithms detect patterns in cost flows and create forecasts. Companies are increasingly setting up project-based and process-based cost centers to respond flexibly to market demands. Especially for temporary projects or agile teams, this development provides more transparency and better control.

Outlook, compliance, and industry-specific solutions

Transparency, compliance, and sustainability are increasingly in focus in cost center management. Companies are adapting their structures to new business models and regulatory requirements. Industry-specific solutions, such as cost center accounting in construction, are gaining importance because they address individual challenges. In the coming years, more cloud-based tools, AI integration, and sustainable cost center strategies can be expected.

Especially if you want to manage cost centers in your company in a targeted way and make processes more efficient, it’s worth taking a look at modern tools like filehub. With automated workflows and a secure, GDPR-compliant platform, you can take your cost center management to the next level—without any programming knowledge. Save time on routine tasks, connect different applications, and always keep full control over your documents.

Try for yourself how simple and practical it is to digitize your cost management—try filehub.one for free now.